When AI Misses an Indemnity Clause: A Connecticut SaaS Tech E&O Claim Walkthrough

When AI Misses an Indemnity Clause: A Connecticut SaaS Tech E&O Claim Walkthrough

The short answer: In early 2025, a Connecticut-based legaltech SaaS startup we work with had its AI-powered contract-review tool fail to flag an open-ended indemnity clause in a Master Service Agreement. The customer — a 200-person logistics company — signed the contract relying on the SaaS tool's "no high-risk clauses detected" summary, and 11 months later got hit with an $1.85M indemnity demand from their own downstream customer. The logistics company turned around and filed a $2.0M claim against the SaaS startup for negligent misrepresentation of an AI-assisted legal analysis. The total claim and defense cost came to $1,425,000 across three policies: the Tech E&O policy paid $1,250,000 in settlement and defense, the Cyber policy paid $135,000 in incident response and forensic AI-model audit costs, and the GL policy paid $40,000 in collateral defense costs for an early jurisdictional motion. The gap that bit the founder: a $250,000 self-insured retention and a sub-limit on AI-specific E&O endorsements he didn't know he had. The whole event is a real-world demonstration of why pre-revenue and early-revenue SaaS founders need the program structure described in our pillar guide on Tech E&O for Connecticut SaaS startups.

The setup

The startup — we'll call it ClauseScout, because the real one asked us not to use its name — is a Series A legaltech SaaS based in West Hartford. Their product is an AI-powered contract-review tool that ingests Master Service Agreements, vendor contracts, and customer agreements, then flags clauses that exceed customer-configured risk thresholds (indemnity caps, IP ownership clauses, exclusivity provisions, termination triggers, etc.). About 60 enterprise customers, $4.2M ARR, 22 employees, fully remote with a small Hartford HQ. They had closed their Series A nine months before the claim hit, at a $32M post-money valuation.

Their insurance program at the time of the loss looked like this: $5M Tech E&O with Hiscox on the StartUp Plus form (the same program we cover in detail in our Hiscox carrier review), $3M standalone Cyber with Beazley, $1M GL through their landlord-required policy with The Hartford, and a $2M D&O policy with Travelers that VC investors had required at the Series A close. Total program premium: roughly $48,000/year. By post-Series A standards, this was a competently built program.

Their typical customer was a mid-market company with 100–500 employees that previously paid an outside law firm $400–$1,200 to review each significant contract. ClauseScout's pitch was simple: same review, 30 seconds, $99 per contract. Customers loved it. The product worked well — most of the time.

The incident

In April 2024, the logistics customer — a 200-person freight forwarder in southern Connecticut — uploaded a 47-page Master Service Agreement from a new manufacturing client into ClauseScout. The AI summary returned in 18 seconds: "No high-risk clauses detected. Indemnity reciprocal and capped at fees paid. Standard limitation-of-liability language. Recommended action: proceed to signature."

The logistics company's contracts manager — who'd been using ClauseScout for nine months — accepted the summary, generated a signature packet, and the CEO signed. Standard workflow. The MSA went into effect May 1, 2024.

What ClauseScout's model missed: an attachment to the MSA — labeled "Schedule C — Indirect Damages Allocation" — that contained an indemnity provision sitting outside the main body of the agreement. The Schedule C clause obligated the logistics company to indemnify the manufacturer for all third-party claims arising from any cargo handled under the agreement, with no cap, no carve-outs, and no notice requirement. It was the kind of language a junior associate at a law firm would catch immediately. The AI didn't.

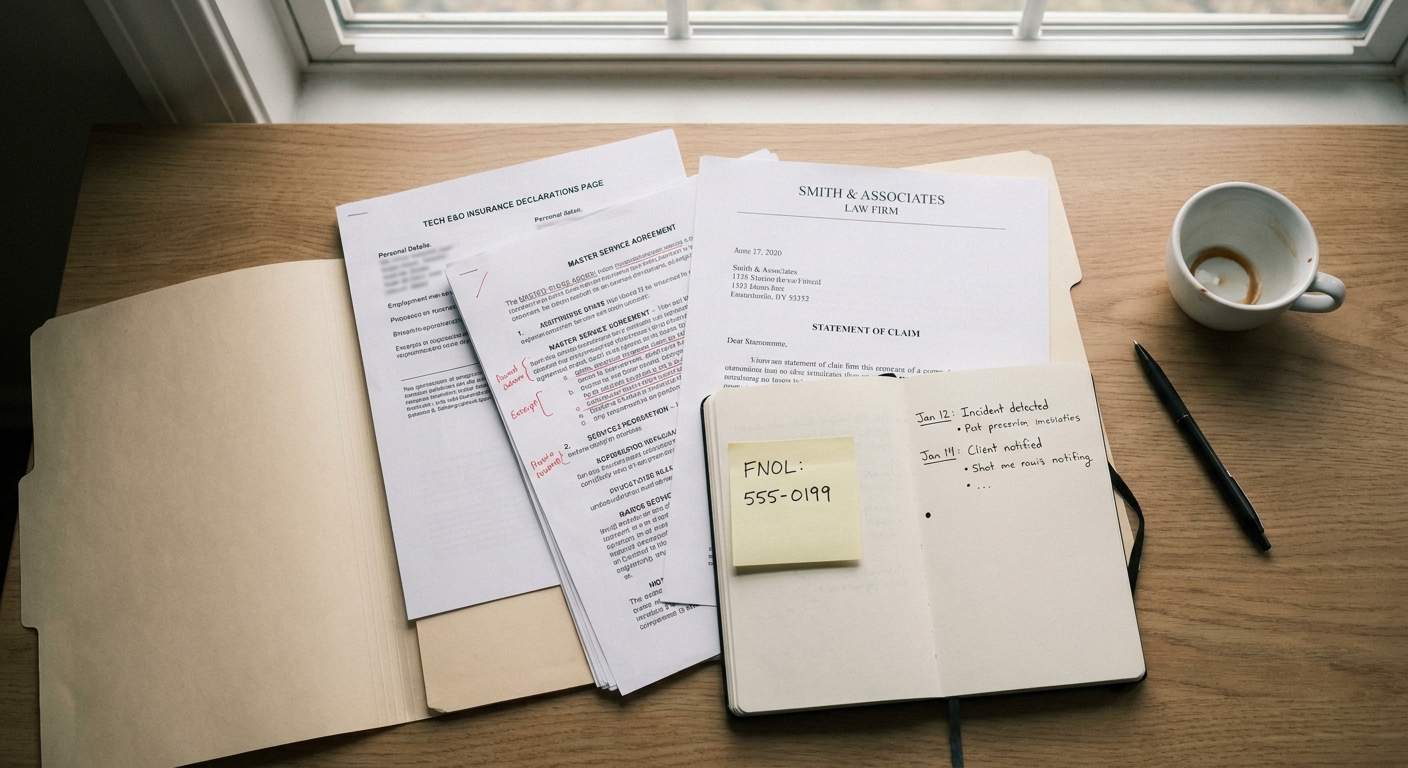

In March 2025, eleven months after the MSA was signed, a shipment of pharmaceutical samples handled under the agreement was rejected at destination as temperature-compromised. The manufacturer's downstream customer — a hospital system — sued the manufacturer for $1.85M in lost samples and study delays. The manufacturer turned around, invoked Schedule C, and demanded full indemnity from the logistics company. The logistics company's general counsel pulled the original MSA, read Schedule C for the first time, looked at ClauseScout's "no high-risk clauses detected" summary in the audit log, and forwarded the whole package to outside counsel with the words: "Find me an angle."

Outside counsel found one. In June 2025, the logistics company filed a $2.0M demand against ClauseScout for negligent misrepresentation, breach of the SaaS service agreement's accuracy warranty, and (in the alternative) gross negligence based on the failure to review attached schedules.

The phone call

The CEO called us at 9:14 AM on a Thursday morning, fifteen minutes after his general counsel finished reading the demand letter aloud to him. The conversation was about 35 minutes:

- FNOL the Tech E&O claim with Hiscox immediately — the core allegation (negligent professional services in delivering an AI-generated legal analysis) is squarely a Tech E&O claim. Do not wait.

- FNOL the Cyber claim with Beazley as a precaution — even though no data was breached, an AI-model integrity failure triggers the "system failure" coverage in the Beazley form and starts the clock on forensic-audit reimbursement.

- Notify D&O at Travelers — not yet a claim against directors and officers, but if the customer's demand metastasizes into investor concerns (it did), the D&O policy may engage later. Preserve the right to notice.

- Preserve everything — the audit log of the original contract upload, the model output, the model version in production at the time, the customer's user-agent and account configuration. Spoliation of AI evidence is a developing legal area.

- Do not communicate directly with the customer's outside counsel — funnel everything through E&O panel counsel that Hiscox will appoint within 72 hours.

We filed E&O and Cyber the same morning. Hiscox panel counsel — a defense litigator at a Hartford firm that specializes in tech professional liability — was on the phone with the CEO by Monday at 10 AM.

What each policy paid

Tech E&O — the core claim: $1,250,000

Hiscox's investigation and defense, plus the eventual settlement, dominated the claim economics. The breakdown:

- Defense costs (8 months): $410,000 — outside counsel hourly fees, expert witness retention (two AI/ML experts, one contract-interpretation expert), document review, motion practice, and a one-day mediation.

- Settlement to the logistics company: $750,000 — mediated settlement at month 9. The plaintiff's nominal demand was $2.0M; their willingness to settle hard reflected the litigation risk on their end (they had also signed the MSA and the gross-negligence alternative count had real defense holes).

- Self-insured retention paid by ClauseScout: $250,000 — applied against the settlement, not in addition. So Hiscox paid $750,000 of the $1.0M total settlement plus the full $410,000 defense, minus the SIR offset.

- Net carrier payout: $1,250,000.

The gap: ClauseScout had a $250,000 SIR on the Tech E&O policy that the founder did not fully understand at the time of bind. A lower SIR ($100,000) was available at bind for an additional $4,200/year in premium. Across two policy years, that would have been $8,400 — versus the $150,000 SIR delta the founder paid out of working capital from his Series A. The SIR is the most-underestimated line item in early-stage E&O programs. We cover this and the other six common pitfalls in 7 Tech E&O Mistakes SaaS Founders Keep Making.

Cyber Policy — system failure and AI-audit costs: $135,000

The Beazley form's "system failure" coverage responded to the AI-model integrity failure even though no third-party data was breached. This is a feature of modern Cyber forms that most founders don't know is there. Beazley paid:

- Forensic AI model audit: $85,000 — third-party ML auditing firm reviewed the model version that produced the failed summary, confirmed the failure mode was an attachment-handling bug rather than malicious tampering or training-data poisoning. Critical to ClauseScout's defense and to the eventual settlement leverage.

- Customer notification and trust-restoration outreach: $32,000 — proactive outreach to all 60 customers explaining the failure mode, what they should re-review, and what fixes were shipped. Cyber-side PR/communications coverage.

- System-restoration costs: $18,000 — engineering hours rebuilding the attachment-handling pipeline and adding redundant clause-detection passes.

Lesson: The Cyber-vs-E&O-vs-GL boundary on AI failures is murky and policy-form-dependent. We unpack this in SaaS Tech E&O vs Cyber vs GL: What Actually Pays When AI Gets It Wrong. The short version: most founders assume Cyber only pays on data breaches. The modern Beazley, Coalition, and At-Bay forms all have system-failure coverage that catches AI-integrity events even without breach.

General Liability — jurisdictional defense costs: $40,000

Early in the litigation, the logistics company's counsel filed in the wrong jurisdiction (Massachusetts, where their downstream customer was, rather than Connecticut where the MSA's forum-selection clause pointed). The Hartford GL form had a defense-coverage extension that responded to the jurisdictional motion costs (about $40,000 across two months and three filings) before the case was transferred to Connecticut state court. After transfer, defense reverted to E&O panel counsel.

Lesson: A SaaS startup's GL policy — usually treated as a checkbox required by a landlord or a Series A term sheet — occasionally engages in real ways at the margins of an E&O dispute. Don't drop GL coverage to save $1,500/year just because "we don't have a physical office."

What didn't pay (and why)

- D&O — never engaged. The logistics company sued the entity, not the founders. If the case had transitioned into a securities-fraud allegation by Series A investors (it did not, but it was close), the D&O policy would have engaged. The notice we filed at FNOL preserved that right.

- Crime / Fidelity Bond — N/A. No employee theft, no social-engineering fraud. ClauseScout did not have a Crime policy.

- Punitive damages — most Tech E&O forms exclude punitives. The mediated settlement did not break punitive language into a separate bucket, so no exclusion was triggered, but it was a real risk if the case had gone to verdict.

- Loss of customer goodwill / lost ARR — no insurance pays for the eight customers (about $310K in ARR) who churned in the six months following the claim becoming public. This is unrecoverable business damage that exceeds the cash payout on the claim itself.

The renewal aftermath

At the next renewal, six months after the settlement closed:

- Tech E&O rate: increased 42% on Hiscox StartUp Plus, with the AI-specific endorsement sub-limit lifted from $1M to $3M and the SIR reduced from $250K to $100K. Net premium went from $24,000 to $41,000.

- Cyber rate: increased 18% on Beazley, partly market trend and partly the system-failure claim. The system-failure sub-limit was lifted from $1M to $2M.

- D&O rate: unchanged. The notice-without-claim didn't trigger a rate action.

- GL: renewed at trend.

- Loss-control remediation: Hiscox required, and ClauseScout implemented, a dual-pass clause-detection system, mandatory schedule-and-attachment review in the product, and a customer-facing disclaimer redesign. Ongoing model-output sampling and external audit cadence were added to the program.

Total renewal program premium went from $48,000 to $74,000. Net cost of the loss event, including the SIR, the lost ARR, the audit and remediation engineering work, and three years of premium increase: roughly $880,000 against a single avoidable miss in the AI's clause-detection pipeline.

What this case study actually teaches

- AI failures are E&O claims first. The legal framing is professional negligence — your software promised X, delivered not-X, and the customer relied on it. That's E&O. Don't let a panicked founder reach for Cyber as the primary policy.

- The SIR is the most-underestimated line. A $250K SIR feels theoretical when the founder is signing the renewal at $24,000 in premium. It feels very real at the moment Hiscox sends an email saying "you owe us the first $250K of the settlement."

- Modern Cyber forms catch AI-integrity events. System-failure coverage exists. It's worth $135K in this case. Read your Cyber form for the words "system failure" or "system disruption" — if they're there, you have coverage no founder thinks they have.

- Notice everything that could engage. The D&O notice cost nothing and preserved future rights. Filing claims and notices early — even precautionary ones — is the broker's job at FNOL and the cheapest insurance asset there is.

- Lost customers cost more than the claim. The cash payout was $1.425M against the program. The unrecoverable ARR was $310K. The damage to founder bandwidth — measured in deal cycles missed and product velocity lost — was uncountable. Insurance pays the bill. It doesn't restore the business.

Beyond insurance: the founder-continuity layer

One additional point worth making — and the reason we built our cousin site Wealth America alongside iConn Insurance Solutions. ClauseScout's claim was recoverable because the company had three policies and a broker who knew how to use them. But the eight months of claim defense consumed roughly 25% of the founder's working time. He missed a CRO hiring cycle, deferred a planned product expansion, and burned cash from a Series A round that was supposed to fund 24 months of runway and instead funded 19.

Insurance covers professional liability and incident response. It doesn't cover the founder's own financial planning when the company's trajectory shifts under him. A claim like this materially affects personal compensation timing, equity vesting acceleration negotiations, secondary-market liquidity, and the founder's family financial plan — none of which the corporate E&O program touches. For a founder whose personal balance sheet is dominated by illiquid startup equity, an integrated wealth-planning view is at least as important as the company's insurance program.

If you want to think about the personal-financial side of running a venture-funded SaaS — what happens to your equity, your tax bill, and your family's cash flow when the company's plans shift — that's the conversation we have on the wealth side. Wealth America is built for founders thinking about that integrated picture.

Frequently Asked Questions About SaaS Tech E&O Claims

Does Tech E&O cover claims that AI got something wrong?

Yes. Tech E&O is designed to cover claims arising from professional services your software delivers, and an AI-generated output that a customer relies on is squarely within scope. Look for an AI-specific endorsement, sub-limits on AI-related claims, and exclusions for "autonomous decisioning."

How much does Tech E&O cost for a Series A SaaS in Connecticut?

Typical 2026 pricing for a $3M–$8M ARR Series A SaaS in Connecticut is $18,000–$55,000 annually for $3M–$5M in limits, depending on revenue, product risk (AI, payments, health-data exposure), and customer mix. Pre-revenue startups can find competent coverage from $4,800/year. Full pricing detail in our cost article linked below.

What's the difference between Tech E&O and Cyber insurance?

Tech E&O covers claims from customers and third parties alleging your software did something wrong professionally. Cyber covers data breach, system failure, ransomware, and incident response on your side. AI-failure events often touch both — Tech E&O is usually the primary; Cyber is the secondary if a "system failure" trigger applies.

How much should I budget for the self-insured retention on a SaaS Tech E&O policy?

Standard SIRs at Series A are $50K–$250K. Pre-revenue SIRs run $5K–$25K. Always reserve cash equal to the SIR in working capital — at claim time, the carrier pays the carrier portion only after you've spent the SIR. Treat it like a deductible you owe in cash up front.

Will my insurance rates go up after a Tech E&O claim?

Yes — typically 30–60% on the affected line for 2–3 years before the loss falls off the experience-rating window. Documented post-loss remediation (model audits, product fixes, ongoing review cadence) can soften the renewal materially. A clean response is worth real money.

Should I tell my customers when an AI-failure incident happens?

Almost always yes, and usually proactively. Cyber-policy crisis-management coverage often pays for the outreach. Customers who learn about an incident from a competitor's sales rep are angrier than customers who learn from a thoughtful email from the founder. Trust restoration is the real outcome.

The bottom line

This was a survivable claim. ClauseScout is still operating, still growing, and the founder still owns roughly the same equity stake he held before the claim hit. But the $250,000 SIR, the lost ARR, the renewal premium increase, and the burned founder bandwidth together cost the company close to $880,000 in pocket money and runway. Better coverage construction — primarily a lower SIR and a richer AI-specific endorsement at bind — would have eliminated about $200,000 of that. The remaining $680,000 was business damage no insurance product can prevent.

If you're a SaaS founder building anything AI-adjacent and you've never walked through what each of your policies would actually pay in a real claim scenario, that's the conversation worth having. Contact iConn Insurance Solutions for a personalized policy review, or visit our sister agency Insure Connecticut LLC for broader Connecticut-startup insurance support. Better to find the gaps now than at 9:14 AM on a Thursday after your general counsel reads a demand letter aloud.